--Disclaimer-- I do not receive any compensation from eDeltaPro. This article is based on my personal opinion.

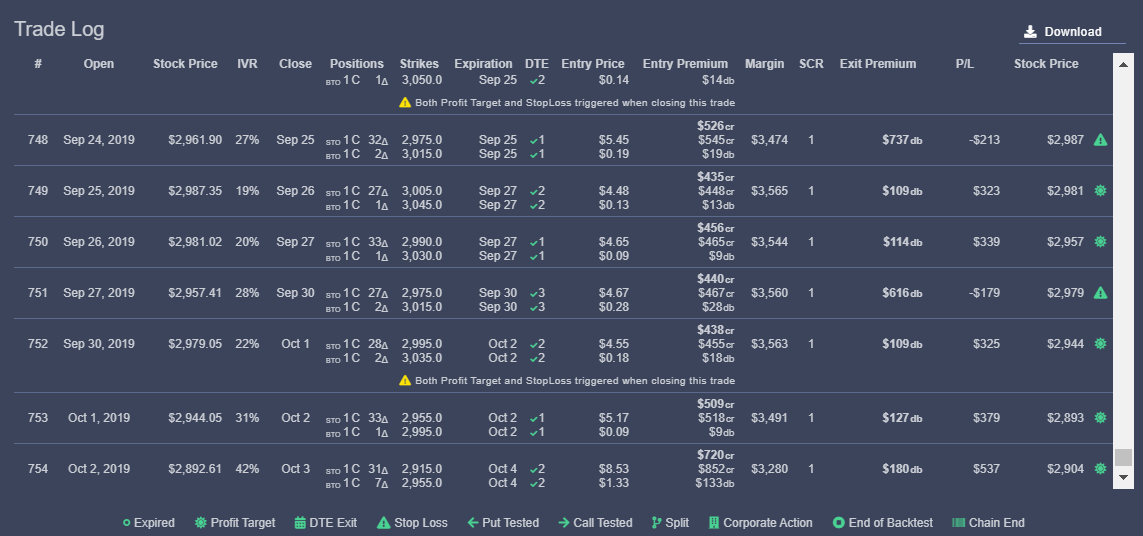

Want to share a very powerful option backtest platform - eDeltaPro. It can backtest almost every mechanical strategy. You can set many parameters such as profit target, stoploss, DTE, rolling, etc. Backtest is supposed to help you to understand your strategy better. In the end of the day, it is still up to your execution ability and trading psychology. If you decide to trade using a mechanical strategy, you have to keep trading it no matter what. You get what the market gives you.

https://www.edeltapro.com/

Before using a backtest platform to evaluate your strategy, you need to consider the following points:

1. Know your product. For example, SPX does not have weekly options until Oct 2005, Monday-expiring options started in Aug 15, 2016, and Wednesday-expiring options started in Feb 23, 2016. So you have much less data points in the past than it is now. The backtest result means differently in the past 3 years vs. 5 years vs. 10 years, etc.

2. I believe every backtest platform only uses EOD data so the result will be much different if you were to enter/exit your position intraday, basically strategies that involve profit target and stoploss .

3. Past result does not guarantee the future performance. Don't be obsessed or over-thinking/explaining the backtest result too much. No one knows what the market will be like in the future. It could be a completely different environment that has never happened before. Sometimes you just get lucky having a good backtest result. For example, you can choose to enter a position everyday and set up the maximum number of simultaneous open position. If you choose to trade daily with long DTE with small maximum open positions, you will skip a lot of trading days. If it is a short put strategy you might just skip the really bad down days of the year and you happen to get great result. But that does not tell you how resilient your strategy is during big selloffs.

Here is an example of Tastytrade's favorite strategy, SPY short naked put 16 delta 45 DTE manage @ 50% and 21 DTE, 12 yr, including commission (Tastyworks rate). It shows that this is a profitable strategy. But if you look at the green trace (unrealized P/L), there is a $10,000 drawdown in the end of 2018. That is where most people give up and decide to take the loss (or get margin call). This is a good example showing why it doesn't matter if you find a profitable strategy from backtest because the problem is execution. Most people will bail out during big loss days. However, this result does not guarantee that you won't see a bigger drawdown in the future. It just tells you the biggest drawdown is 13.7% with this strategy in the past 12 years.

For an ideal strategy, you should be looking for a smooth P/L curve. For example, 60 delta short strangle managed @10% looks very promising. But you do need a lot of capital to do that. The capital req. showed in the picture is the lowest starting capital. The program will fully utilize BP including the profit. One thing to note is that this strategy only gives you 300% ROC (return on capital) over 12 years and this is the maximum ROC you can get since it fully utilizes the capital. 300% ROC over 12 years I would rather just buy and hold SPY. ROC is a big thing to consider. I would argue if your strategy does not give you a better ROC than holding SPY, it is not worth the effort to execute it.

To summarize, backtest can quickly tell you if one strategy has potential or not as well as help you to understand what to expect with the strategy (like potential consecutive losses, etc). It does have limitations if you want to incorporate more complex defense strategies. I personally use it to educate myself.